Note

Download this Jupyter notebook and all

data

(unzip next to the ipynb file!).

You will need a Gurobi license to run this notebook, please follow the

license instructions.

Leverage by Borrowing Cash¶

The standard mean-variance (Markowitz) portfolio selection model determines an optimal investment portfolio that balances risk and expected return. In this notebook, we maximize the portfolio’s expected return while constraining the admissible variance (risk) to a given maximum level. Please refer to the annotated list of references for more background information on portfolio optimization.

To this basic model, we add leverage. Leverage means borrowing capital from a third party to buy more assets (and paying interest on the borrowed capital). This magnifies both the potential upside and downside.

[2]:

import gurobipy as gp

import pandas as pd

import numpy as np

import matplotlib.pyplot as plt

Input Data¶

The following input data is used within the model:

\(S\): set of stocks

\(\mu\): vector of expected returns

\(\Sigma\): PSD variance-covariance matrix

\(\sigma_{ij}\) covariance between returns of assets \(i\) and \(j\)

\(\sigma_{ii}\) variance of return of asset \(i\)

[4]:

# Import some example data set

Sigma = pd.read_pickle("sigma.pkl")

mu = pd.read_pickle("mu.pkl")

Formulation¶

Mathematically, this results in a convex quadratically constrained optimization problem.

Model Parameters¶

The following parameters are used within the model:

\(\bar\sigma^2\): maximal admissible variance for the portfolio return

\(c_\text{rf}\): interest on the risk-free asset. For simplicity, we assume the same interest rate for lending and borrowing.

\(\ell_\text{rf}\): maximal short on risk-free asset

\(u_\text{rf}\): maximal investment in risk-free asset

[5]:

# Values for the model parameters:

V = 4.0 # Maximal admissible variance (sigma^2)

c_rf = 2 / 52 # interest rate on risk-free asset

l_rf = -0.3 # maximal borrowing of risk-free asset

u_rf = 1 # maximal investment in risk-free asset

Decision Variables¶

We require two types of decision variables:

The proportions of capital invested among the considered stocks. The corresponding vector of positions is denoted by \(x\) with its component \(x_i\) denoting the proportion of capital invested in stock \(i\).

The proportion \(x_\text{rf}\) invested in the risk-free asset. This may be positive or negative. If positive, we gain a risk-free return; if negative, we pay interest on the borrowed amount.

Variable Bounds¶

Each position must be nonnegative:

The risk-free position must be within its bounds:

Setting the upper bound \(u_\text{rf}=1\) means the portfolio is allowed to be fully invested in the risk-free asset.

[6]:

%%capture

# Create an empty optimization model

m = gp.Model()

# Add variables: x[i] denotes the proportion invested in stock i

x = m.addMVar(len(mu), name="x")

# Risk-free allocation

x_rf = m.addVar(lb=l_rf, ub=u_rf, name="x_rf")

Constraints¶

The budget constraint ensures that all capital (both initial and borrowed) is invested:

The estimated risk must not exceed a prespecified maximal admissible level of variance \(\bar\sigma^2\):

[7]:

%%capture

# Budget constraint: all investments sum up to 1

m.addConstr(x.sum() + x_rf == 1, name="Budget_Constraint")

# Upper bound on variance

risk_constr = m.addConstr(x @ Sigma.to_numpy() @ x <= V, name="Variance")

Objective Function¶

The objective is to maximize the expected return of the portfolio. We need to account for risk-free returns and costs for borrowing cash: \begin{equation*} \max_x \underbrace{c_\text{rf} x_\text{rf}}_{\substack{\text{cost for borrowing}\\\text{or risk-free return}}} + \underbrace{\mu^\top x}_\text{expected return from stocks} \end{equation*}

[8]:

m.setObjective(c_rf * x_rf + mu.to_numpy() @ x, gp.GRB.MAXIMIZE)

We now solve the optimization problem:

[9]:

m.optimize()

Gurobi Optimizer version 13.0.2 build v13.0.2rc1 (linux64 - "Ubuntu 24.04.4 LTS")

CPU model: AMD EPYC 7763 64-Core Processor, instruction set [SSE2|AVX|AVX2]

Thread count: 1 physical cores, 2 logical processors, using up to 2 threads

WLS license 2443533 - registered to Gurobi GmbH

Optimize a model with 1 rows, 463 columns and 463 nonzeros (Max)

Model fingerprint: 0xc5359fbf

Model has 463 linear objective coefficients

Model has 1 quadratic constraint

Coefficient statistics:

Matrix range [1e+00, 1e+00]

QMatrix range [3e-03, 1e+02]

Objective range [4e-02, 6e-01]

Bounds range [3e-01, 1e+00]

RHS range [1e+00, 1e+00]

QRHS range [4e+00, 4e+00]

Presolve time: 0.03s

Presolved: 463 rows, 926 columns, 107878 nonzeros

Presolved model has 1 second-order cone constraint

Ordering time: 0.01s

Barrier statistics:

AA' NZ : 1.070e+05

Factor NZ : 1.074e+05 (roughly 1 MB of memory)

Factor Ops : 3.319e+07 (less than 1 second per iteration)

Threads : 1

Objective Residual

Iter Primal Dual Primal Dual Compl Time

0 1.35263322e+01 1.38517017e+00 5.74e+01 5.93e-02 4.06e-02 0s

1 1.72294179e+00 1.45034312e+00 5.96e+00 6.53e-08 5.06e-03 0s

2 5.65980685e-01 7.13794601e-01 1.23e+00 5.20e-09 1.14e-03 0s

3 2.76492884e-01 4.52651953e-01 1.35e-06 9.08e-10 1.90e-04 0s

4 3.04811140e-01 3.88375383e-01 1.49e-12 2.76e-10 9.00e-05 0s

5 3.32848350e-01 3.72022345e-01 1.44e-15 4.16e-16 4.22e-05 0s

6 3.60987566e-01 3.62373983e-01 3.11e-15 2.78e-17 1.49e-06 0s

7 3.61633548e-01 3.61707202e-01 2.89e-15 1.11e-16 7.94e-08 0s

8 3.61665207e-01 3.61667012e-01 8.88e-16 1.58e-15 1.94e-09 0s

9 3.61665648e-01 3.61666258e-01 6.48e-14 1.36e-13 6.56e-10 0s

Barrier solved model in 9 iterations and 0.25 seconds (0.59 work units)

Optimal objective 3.61665648e-01

Display basic solution data for all non-negligible positions; for clarity we’ve rounded all solution quantities to five digits.

[10]:

print(f"Expected return: {m.ObjVal:.6f}")

print(f"Variance: {x.X @ Sigma @ x.X:.6f}")

print(f"Solution time: {m.Runtime:.2f} seconds\n")

print(f"Total investment: {x.X[x.X>1e-5].sum():.6f}")

print(f"Risk-free allocation: {x_rf.X:.6f}")

print(f"Number of positions: {np.count_nonzero(x.X[abs(x.X)>1e-5])}")

# Print all assets with a non-negligible position

df = pd.DataFrame(

index=mu.index,

data={

"x": x.X,

},

).round(6)

df[(abs(df["x"]) > 1e-5)].sort_values("x", ascending=False)

Expected return: 0.361666

Variance: 3.999995

Solution time: 0.25 seconds

Total investment: 1.180835

Risk-free allocation: -0.180836

Number of positions: 31

[10]:

| x | |

|---|---|

| LLY | 0.234514 |

| PGR | 0.130495 |

| KDP | 0.109867 |

| TMUS | 0.061023 |

| NVDA | 0.059568 |

| KR | 0.059165 |

| DPZ | 0.058688 |

| TTWO | 0.052528 |

| WM | 0.049898 |

| NOC | 0.049281 |

| ODFL | 0.039805 |

| ORLY | 0.035924 |

| AVGO | 0.034771 |

| WST | 0.029062 |

| MSFT | 0.027460 |

| ED | 0.018787 |

| MKTX | 0.018729 |

| AZO | 0.018145 |

| MNST | 0.015005 |

| CLX | 0.014785 |

| META | 0.013694 |

| HRL | 0.010083 |

| NFLX | 0.009696 |

| WMT | 0.008265 |

| UNH | 0.007742 |

| XEL | 0.004691 |

| DXCM | 0.004483 |

| CBOE | 0.003388 |

| MOH | 0.000747 |

| WEC | 0.000449 |

| CME | 0.000096 |

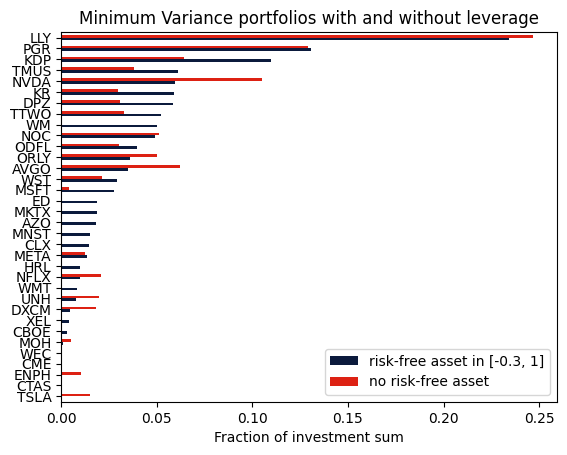

Comparison with the unconstrained portfolio without leverage¶

We can also compute the portfolio without leverage and compare the resulting portfolios.

[11]:

# adjust RHS of short constraint

x_rf.lb = 0

x_rf.ub = 0

m.params.OutputFlag = 0

m.optimize()

# retrieve and display solution data

mask = (abs(df["x"]) > 1e-5) | (x.X > 1e-5)

df2 = pd.DataFrame(

index=df["x"][mask].index,

data={

"risk-free asset in [-0.3, 1]": df["x"],

"no risk-free asset": x.X[mask],

},

).sort_values(by=["risk-free asset in [-0.3, 1]"], ascending=True)

axs = df2.plot.barh(color=["#0b1a3c", "#dd2113"])

axs.set_xlabel("Fraction of investment sum")

plt.title("Minimum Variance portfolios with and without leverage")

plt.show()

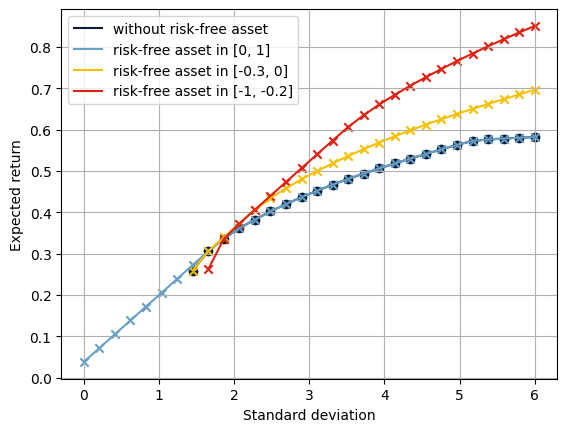

Efficient Frontiers¶

The efficient frontier reveals the balance between risk and return in investment portfolios. It shows the best-expected return level that can be achieved for a specified risk level. We compute this by solving the above optimization problem for a sample of admissible risk levels with and without the risk-free asset. When we restrict investment amounts in the risk-free asset, that is \(u_\text{rf} < 1\), the model may be infeasible for very small risk levels.

[12]:

risks = np.linspace(0, 6, 30)

rf_bnds = [(0, 0), (0, 1), (-0.3, 0), (-1, -0.2)]

returns = pd.DataFrame(index=risks)

# prevent Gurobi log output

m.params.OutputFlag = 0

for lb, ub in rf_bnds:

name = f"[{lb}, {ub}]"

x_rf.LB = lb

x_rf.UB = ub

r = np.zeros(risks.shape)

# solve the model for each risk level

for i, risk_level in enumerate(risks):

# set risk level: RHS of risk constraint

risk_constr.QCRHS = risk_level**2

m.optimize()

# check status and store data

if m.Status == gp.GRB.OPTIMAL:

r[i] = m.ObjVal

else:

r[i] = float("NaN")

returns[name] = r

We can display the efficient frontiers for all strategies. We plot the expected returns (on the \(y\)-axis) against the standard deviation \(\sqrt{x^\top\Sigma x}\) of the expected returns (on the \(x\)-axis).

[13]:

colors = ["#0b1a3c", "#67a1c3", "#f6c105", "#dd2113"]

markers = ["o", "x", "x", "x"]

fig, axs = plt.subplots()

for column, color, marker in zip(returns.columns, colors, markers):

axs.scatter(x=returns.index, y=returns[column], marker=marker, color=color)

label = (

"without risk-free asset"

if column == "[0, 0]"

else f"risk-free asset in {column}"

)

axs.plot(

returns.index,

returns[column],

label=label,

color=color,

)

axs.set_xlabel("Standard deviation")

axs.set_ylabel("Expected return")

axs.legend()

axs.grid()

plt.show()

If we allow investing in a risk-free asset, the portfolio variance can be arbitrarily small. If one invests all capital into the risk-free asset, the variance (and standard deviation) is 0. Without that possibility (i.e., \(x_\text{rf}\leq 0\)), the minimal possible risk is greater than 0. If we can invest in the risk-free asset, the left-most part of the efficient frontier is a straight line from the portfolio that invests the entire capital into the risk-free asset to the minimal-variance portfolio. If we allow higher risk, including the ability to borrow cash, this shifts the efficient frontier towards higher returns.

Takeaways¶

Leverage can be modeled by adding a variable for the risk-free portion that can take negative values.

Different strategies can be tested by modifying bounds and right-hand sides; there is no need to rebuild the model.