Note

Download this Jupyter notebook and all

data

(unzip next to the ipynb file!).

You will need a Gurobi license to run this notebook, please follow the

license instructions.

Sector Allocation¶

The standard mean-variance (Markowitz) portfolio selection model determines an optimal investment portfolio that balances risk and expected return. In this notebook, we minimize the variance (risk) of the portfolio given that the prescribed level of expected return is attained. Please refer to the annotated list of references for more background information on portfolio optimization.

The stock market comprises different sectors (Technology, Financial Services, Healthcare, etc.), industry groups, industries, and sub-industries and one often wants to limit exposure to each of them. In order to diversify investment risks across different industries, or to comply with regulatory requirements, one often needs to add sector allocation constraints to the basic model to limit

the number of open positions and

the total investment

in each sector.

[2]:

import gurobipy as gp

import gurobipy_pandas as gppd

import pandas as pd

import numpy as np

import matplotlib.pyplot as plt

Input Data¶

The following input data is used within the model:

\(S\): set of stocks

\(\mu\): vector of expected returns

\(\Sigma\): PSD variance-covariance matrix

\(\sigma_{ij}\) covariance between returns of assets \(i\) and \(j\)

\(\sigma_{ii}\) variance of return of asset \(i\)

\(M\): set of sectors. We use the 11 sectors in the Global Industry Classification Standard (GICS) classification.

[4]:

# Import some example data set

Sigma = pd.read_pickle("sigma.pkl")

mu = pd.read_pickle("mu.pkl")

We also import some data that contains the market capitalization and sector according to the GICS hierarchy for each of the stocks. We will need the total market capitalization and relative weight of each sector in the index.

[5]:

# Import stock data

data = pd.read_pickle("stock_data.pkl")

# Display sector data

sectors = (

data[["Sector", "MarketCap"]].groupby(by=["Sector"]).aggregate(["sum", "count"])

)

sectors.columns = ["MarketCap", "Number"]

sectors["Weight"] = sectors["MarketCap"] / sectors["MarketCap"].sum()

sectors.sort_values("MarketCap", ascending=False)

[5]:

| MarketCap | Number | Weight | |

|---|---|---|---|

| Sector | |||

| Technology | 12715607901184 | 65 | 0.286058 |

| Communication Services | 6054451107840 | 18 | 0.136205 |

| Financial Services | 5588576733184 | 64 | 0.125724 |

| Healthcare | 5272300330496 | 60 | 0.118609 |

| Consumer Cyclical | 4588151685632 | 53 | 0.103218 |

| Industrials | 3305283061760 | 67 | 0.074358 |

| Consumer Defensive | 2780607703040 | 34 | 0.062554 |

| Energy | 1569043430400 | 23 | 0.035298 |

| Real Estate | 931872515072 | 29 | 0.020964 |

| Utilities | 868188347904 | 29 | 0.019531 |

| Basic Materials | 777054908928 | 20 | 0.017481 |

For example, 65 stocks from our set belong to the Technology sector, which accounts for 28.6% of the total market capitalization.

For reference, we will compute the market portfolio as the portfolio that allocates into all stocks relative to the stocks’ market capitalization.

[6]:

x_market = data["MarketCap"] / data["MarketCap"].sum()

data_market = {

"Variance": x_market @ Sigma @ x_market,

"Expected return": x_market @ mu,

}

print(data_market)

{'Variance': np.float64(4.673079099420153), 'Expected return': np.float64(0.28157962440870105)}

Formulation¶

The model minimizes the variance of the portfolio subject to

the portfolio matches the expected return of the market portfolio,

the size of each position does not fall below a certain level,

the total investment in each sector lies between specified lower and upper bounds,

the number of positions in each sector does not exceed a specified number.

Mathematically, this results in a convex quadratic mixed-integer optimization problem.

Model Parameters¶

We use the following parameters:

\(\bar\mu\): required expected portfolio return

\(\ell>0\): lower bound on position size

\(K_m\): maximal number of stocks in the portfolio from sector \(m\).

\(\ell_m, u_m\): lower and upper bounds on the weight of sector \(m\) in the portfolio. In this notebook, we will choose those bounds as a +/- 10% envelope around the sector weight in the S&P 500: That is, we choose \(\ell_m = (1-\delta)w_m, u_m = (1+\delta)w_m\), where \(w_m\) is the weight of sector \(m\) in the index.

[7]:

# Values for the model parameters:

r = data_market["Expected return"] # Required return

l = 0.00001 # Minimal position size

K = 3 # Maximal number of stocks per sector

delta = 0.1 # bound on the relative deviation from sector weight

Decision Variables¶

We need two sets of decision variables:

The proportions of capital invested among the considered stocks. The corresponding vector of positions is denoted by \(x\) with its component \(x_i\) denoting the proportion of capital invested in stock \(i\).

Binary variables \(b_i\) indicating whether or not asset \(i\) is held. If \(b_i\) is 0, the holding \(x_i\) is also 0; otherwise if \(b_i\) is 1, the investor holds asset \(i\) (that is, \(x_i \geq \ell\)).

Variable Bounds¶

Each position must be between 0 and 1; this prevents leverage and short-selling:

\begin{equation*} 0\leq x_i\leq 1 \; , \; i \in S \end{equation*}

The \(b_i\) must be binary:

\begin{equation*} b_i \in \{0,1\} \; , \; i \in S \end{equation*}

We will model this using the gurobipy-pandas package. Using this, we create a DataFrame containing the decision variables as columns.

[8]:

# Create an empty optimization model

m = gp.Model()

# Add variables to model, align with data

df_model = (

# x[i] denotes the proportion invested in stock i

data.gppd.add_vars(m, name="x", ub=1)

# b[i]=1 if stock i is held, and b[i]=0 otherwise

.gppd.add_vars(m, name="b", vtype=gp.GRB.BINARY).drop(

"Risk", axis=1

) # Not needed here

)

# A quick look at this DataFrame:

m.update()

df_model

[8]:

| MarketCap | Sector | Name | x | b | |

|---|---|---|---|---|---|

| MSFT | 3004349808640 | Technology | Microsoft Corporation | <gurobi.Var x[MSFT]> | <gurobi.Var b[MSFT]> |

| AAPL | 2893580337152 | Technology | Apple Inc. | <gurobi.Var x[AAPL]> | <gurobi.Var b[AAPL]> |

| AMZN | 1750173089792 | Consumer Cyclical | Amazon.com, Inc. | <gurobi.Var x[AMZN]> | <gurobi.Var b[AMZN]> |

| NVDA | 1684540096512 | Technology | NVIDIA Corporation | <gurobi.Var x[NVDA]> | <gurobi.Var b[NVDA]> |

| GOOGL | 1789200171008 | Communication Services | Alphabet Inc. | <gurobi.Var x[GOOGL]> | <gurobi.Var b[GOOGL]> |

| ... | ... | ... | ... | ... | ... |

| RL | 9448713216 | Consumer Cyclical | Ralph Lauren Corporation | <gurobi.Var x[RL]> | <gurobi.Var b[RL]> |

| SEE | 4919490560 | Consumer Cyclical | Sealed Air Corporation | <gurobi.Var x[SEE]> | <gurobi.Var b[SEE]> |

| DVA | 10014481408 | Healthcare | DaVita Inc. | <gurobi.Var x[DVA]> | <gurobi.Var b[DVA]> |

| ALK | 4465086464 | Industrials | Alaska Air Group, Inc. | <gurobi.Var x[ALK]> | <gurobi.Var b[ALK]> |

| MHK | 6813997568 | Consumer Cyclical | Mohawk Industries, Inc. | <gurobi.Var x[MHK]> | <gurobi.Var b[MHK]> |

462 rows × 5 columns

Constraints¶

The budget constraint ensures that all capital is invested:

\begin{equation*} \sum_{i \in S} x_i =1 \end{equation*}

The expected return of the portfolio must be at least \(\bar\mu\):

\begin{equation*} \mu^\top x \geq \bar\mu \end{equation*}

We use functionality from pandas to create those constraints. Note that this ensures that the indices of df_model and mu are aligned.

[9]:

%%capture

# Budget constraint: all investments sum up to 1

m.addConstr(df_model["x"].sum() == 1, name="Budget_Constraint")

# Lower bound on expected return

m.addConstr(mu @ df_model["x"] >= r, "Required_Return")

From the bounds alone, \(x\) can take any value between \(0\) and \(1\). To enforce the minimal position size, we need the binary variables \(b\) and the following sets of discrete constraints:

Ensure that \(x_i = 0\) if \(b_i = 0\):

\begin{equation*} x_i \leq b_i \; , \; i \in S\tag{1} \end{equation*}

Note that since \(x_i\) has an upper bound of 1, the above constraint is non-restrictive if \(b_i = 1\).

Ensure a minimal position size of \(\ell\) if asset \(i\) is traded:

\begin{equation*} x_i \geq \ell b_i \; , \; i \in S\tag{2} \end{equation*}

Hence \(b_i = 1\) implies \(x_i \geq \ell\). Additionally, if \(b_i = 0\), the above constraint is non-restrictive since \(x_i\) has a lower bound of 0.

To add these constraints to the model, we use gurobipy-pandas functionality.

[10]:

%%capture

# Force x to 0 if not traded; see formula (1) above

# We use a gurobipy-pandas DataFrame accessor that takes the constraint as a string with column labels

df_model.gppd.add_constrs(m, "x <= b", name="Indicator")

# Minimal position; see formula (2) above

# We use a gurobipy-pandas function that takes the model, the left-hand side, sense, and right-hand side

gppd.add_constrs(

m,

df_model["x"],

">",

l * df_model["b"],

name="Minimal_Position",

)

Allocation constraints by sector¶

The weight of all stocks in sector \(m\) must be within the prescribed bounds:

\begin{equation*} \ell_m \leq \sum_{i\in m} x_i \leq u_m \; , \; m \in M\; , \tag{3} \end{equation*}

where \(\ell_m = (1-\delta)w_m\) and \(u_m = (1+\delta)w_m\).

Likewise, the number of stocks in sector \(m\) must not exceed \(K_m\). We use the binary variables \(b_i\) to count positions.

\begin{equation*} \sum_{i\in m} b_i \leq K_m \; , \; m \in M \tag{4} \end{equation*}

The DataFrame’s groupby method can be used to conveniently create sums over all stocks within the same sector:

[11]:

# Lower and upper bounds on position size per sector; see formula (3) above

sector_weight_ub = gppd.add_constrs(

m,

df_model.groupby("Sector")["x"].sum(),

"<",

sectors["Weight"] * (1 + delta),

name="Sector_Weight_UB",

)

sector_weight_lb = gppd.add_constrs(

m,

df_model.groupby("Sector")["x"].sum(),

">",

sectors["Weight"] * (1 - delta),

name="Sector_Weight_LB",

)

# Upper bound on the number of positions per sector; see formula (4) above

sector_cardinality = gppd.add_constrs(

m,

df_model.groupby("Sector")["b"].sum(),

"<",

K,

name="Sector_Cardinality",

)

Objective Function¶

The objective is to minimize the risk of the portfolio, which is measured by its variance:

\begin{equation*} \min_x x^\top \Sigma x \end{equation*}

[12]:

# Define objective function: Minimize risk

m.setObjective(df_model["x"] @ Sigma @ df_model["x"], gp.GRB.MINIMIZE)

We now solve the optimization problem:

[13]:

m.optimize()

Gurobi Optimizer version 13.0.2 build v13.0.2rc1 (linux64 - "Ubuntu 24.04.4 LTS")

CPU model: AMD EPYC 7763 64-Core Processor, instruction set [SSE2|AVX|AVX2]

Thread count: 1 physical cores, 2 logical processors, using up to 2 threads

WLS license 2443533 - registered to Gurobi GmbH

Optimize a model with 959 rows, 924 columns and 4158 nonzeros (Min)

Model fingerprint: 0xd130e4c6

Model has 0 linear objective coefficients

Model has 106953 quadratic objective terms

Variable types: 462 continuous, 462 integer (462 binary)

Coefficient statistics:

Matrix range [1e-05, 1e+00]

Objective range [0e+00, 0e+00]

QObjective range [6e-03, 2e+02]

Bounds range [1e+00, 1e+00]

RHS range [2e-02, 3e+00]

Presolve time: 0.04s

Presolved: 959 rows, 924 columns, 4157 nonzeros

Presolved model has 106953 quadratic objective terms

Variable types: 462 continuous, 462 integer (462 binary)

Found heuristic solution: objective 4.2808136

Root relaxation: objective 2.599011e+00, 210 iterations, 0.01 seconds (0.01 work units)

Nodes | Current Node | Objective Bounds | Work

Expl Unexpl | Obj Depth IntInf | Incumbent BestBd Gap | It/Node Time

0 0 2.59901 0 36 4.28081 2.59901 39.3% - 0s

H 0 0 2.6251831 2.59901 1.00% - 0s

H 0 0 2.6229197 2.59901 0.91% - 0s

H 0 0 2.6225600 2.59901 0.90% - 0s

0 0 2.59901 0 33 2.62256 2.59901 0.90% - 0s

0 0 2.59901 0 33 2.62256 2.59901 0.90% - 0s

0 0 2.59901 0 33 2.62256 2.59901 0.90% - 0s

0 0 2.59901 0 33 2.62256 2.59901 0.90% - 0s

0 0 2.59901 0 33 2.62256 2.59901 0.90% - 0s

0 0 2.59901 0 33 2.62256 2.59901 0.90% - 0s

0 2 2.59901 0 33 2.62256 2.59901 0.90% - 0s

H 135 38 2.6225597 2.60080 0.83% 5.1 0s

Cutting planes:

Gomory: 1

Cover: 2

Implied bound: 1

MIR: 6

Flow cover: 11

Explored 485 nodes (2670 simplex iterations) in 0.79 seconds (0.72 work units)

Thread count was 2 (of 2 available processors)

Solution count 5: 2.62256 2.62256 2.62292 ... 4.28081

Optimal solution found (tolerance 1.00e-04)

Best objective 2.622559688764e+00, best bound 2.622301879441e+00, gap 0.0098%

Display basic solution data based on the individual assets and sectors:

[14]:

data_model1 = {

"Variance": m.ObjVal,

"Expected return": mu @ df_model["x"].gppd.X,

}

print(f"Variance: {m.ObjVal:.6f}")

print(f"Expected return: {mu @ df_model['x'].gppd.X:.6f}")

print(f"Solution time: {m.Runtime:.2f} seconds\n")

# Print investments (with non-negligible value, i.e. >1e-5)

data["Position"] = df_model["x"].gppd.X

data[data["Position"] > 1e-5][["MarketCap", "Sector", "Position"]].sort_values(

"Position", ascending=False

)

Variance: 2.622560

Expected return: 0.281580

Solution time: 0.79 seconds

[14]:

| MarketCap | Sector | Position | |

|---|---|---|---|

| MSFT | 3004349808640 | Technology | 0.129882 |

| LLY | 667918204928 | Healthcare | 0.119143 |

| PGR | 106073907200 | Financial Services | 0.096290 |

| BR | 23238772736 | Technology | 0.082739 |

| TMUS | 193721221120 | Communication Services | 0.063901 |

| DPZ | 14603976704 | Consumer Cyclical | 0.054687 |

| WM | 75618992128 | Industrials | 0.049627 |

| TYL | 17882144768 | Technology | 0.044831 |

| AZO | 48049000448 | Consumer Cyclical | 0.037813 |

| TTWO | 27903057920 | Communication Services | 0.035356 |

| NOC | 66327912448 | Industrials | 0.031669 |

| KR | 33348851712 | Consumer Defensive | 0.030470 |

| CME | 73643769856 | Financial Services | 0.029367 |

| KDP | 43670155264 | Consumer Defensive | 0.024210 |

| CTRA | 18142871552 | Energy | 0.023883 |

| VZ | 174259945472 | Communication Services | 0.023327 |

| ED | 31142295552 | Utilities | 0.021474 |

| MCD | 207836446720 | Consumer Cyclical | 0.020241 |

| DLR | 44423024640 | Real Estate | 0.018868 |

| HRL | 16470820864 | Consumer Defensive | 0.014130 |

| MKTX | 8191925760 | Financial Services | 0.012639 |

| APD | 49082589184 | Basic Materials | 0.008529 |

| XOM | 402421940224 | Energy | 0.007886 |

| NEM | 38533505024 | Basic Materials | 0.007204 |

| GILD | 95658491904 | Healthcare | 0.006410 |

| MRK | 318729060352 | Healthcare | 0.004917 |

| RSG | 54473105408 | Industrials | 0.000497 |

[15]:

# Display sector data

data_sectors = (

data[data["Position"] > 1e-5].groupby("Sector")["Position"].agg(["sum", "count"])

)

data_sectors.columns = ["Weight", "Number"]

data_sectors.sort_values("Weight", ascending=False)

[15]:

| Weight | Number | |

|---|---|---|

| Sector | ||

| Technology | 0.257452 | 3 |

| Financial Services | 0.138296 | 3 |

| Healthcare | 0.130470 | 3 |

| Communication Services | 0.122584 | 3 |

| Consumer Cyclical | 0.112741 | 3 |

| Industrials | 0.081793 | 3 |

| Consumer Defensive | 0.068810 | 3 |

| Energy | 0.031768 | 2 |

| Utilities | 0.021474 | 1 |

| Real Estate | 0.018868 | 1 |

| Basic Materials | 0.015733 | 2 |

Comparison with the unconstrained portfolio¶

For comparison purposes, we will also compute the portfolio without the sector allocation constraints:

upper and lower bounds on the weight of each sector in the portfolio,

upper bound on the number of bought stocks in each sector.

To compute this, we relax the right-hand sides of those constraints enough to make them non-binding. In addition, we show the risk and return of the market porfolio that results from weighing all the of S&P500 stocks according to their market capitalization.

[16]:

# remove sector allocation constraints by relaxing the RHSs

sector_weight_ub.gppd.set_attr("RHS", 1)

sector_weight_lb.gppd.set_attr("RHS", 0)

sector_cardinality.gppd.set_attr("RHS", 100)

m.params.OutputFlag = 0

m.optimize()

data_model2 = {

"Variance": m.ObjVal,

"Expected return": mu @ df_model["x"].gppd.X,

}

df_results = pd.DataFrame(

index=["with allocation constraints", "unconstrained", "market"],

data=[data_model1, data_model2, data_market],

)

display(df_results)

| Variance | Expected return | |

|---|---|---|

| with allocation constraints | 2.622560 | 0.28158 |

| unconstrained | 2.344234 | 0.28158 |

| market | 4.673079 | 0.28158 |

From this comparison we see the effect of enforcing our sector allocation constraints:

In comparison with the unconstrained portfolio, the variance increases by about 15% by enforcing all sector allocation constraints. This is the “price” we have to pay for these portfolio features.

The optimized portfolios have greatly reduced variance in comparison with the market portfolio.

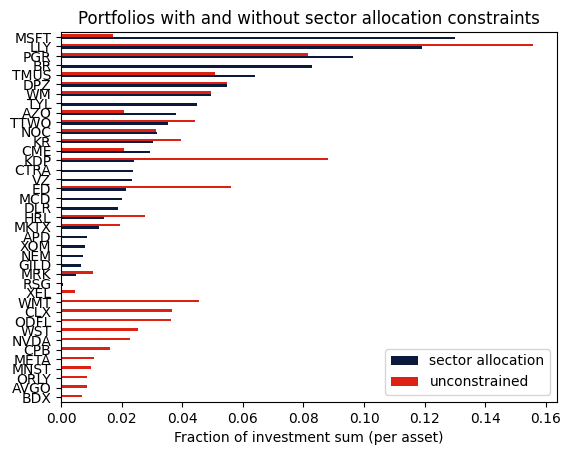

Finally we visualize the allocated investment sum for each stock being bought by either of the two optimized portfolios.

[17]:

# retrieve solution data and store in data

data["Position unconstr"] = df_model["x"].gppd.X

mask = (data["Position"] > 1e-5) | (data["Position unconstr"] > 1e-5)

df_positions = pd.DataFrame(

index=data[mask].index,

data={

"sector allocation": data["Position"],

"unconstrained": data["Position unconstr"],

},

).sort_values(by=["sector allocation", "unconstrained"], ascending=True)

# plot data

axs = df_positions.plot.barh(color=["#0b1a3c", "#dd2113"])

axs.set_xlabel("Fraction of investment sum (per asset)")

plt.title("Portfolios with and without sector allocation constraints")

plt.show()

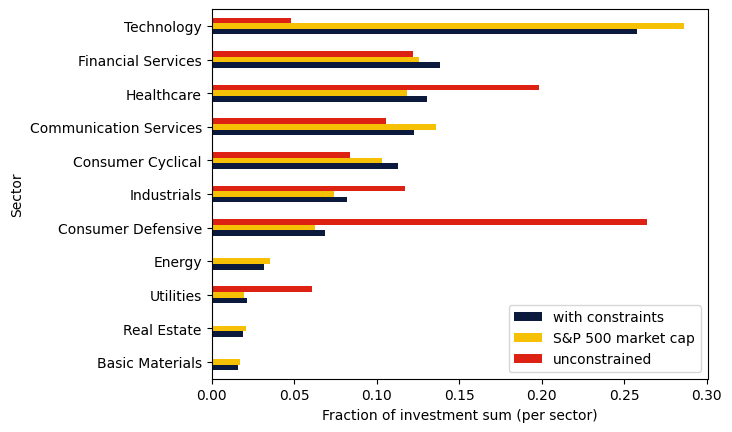

We can also compare the resulting sector allocation with the unconstrained portfolio and the market capitalization in the S&P 500 index:

[18]:

df_sectors = pd.DataFrame(

index=data_sectors.index,

data={

"with constraints": data_sectors["Weight"],

"S&P 500 market cap": sectors["Weight"],

"unconstrained": data.groupby("Sector").sum()["Position unconstr"],

},

).sort_values(by=["with constraints"], ascending=True)

axs = df_sectors.plot.barh(color=["#0b1a3c", "#f6c105", "#dd2113"])

axs.set_xlabel("Fraction of investment sum (per sector)")

plt.show()

One can see that without the allocation constraints, the resulting portfolio can be quite far from the distribution in the index. For example, in the S&P 500, the Technology sector has a weight of almost 29%, but the unconstrained portfolio almost completely avoids it due to its high variance. With the sector allocation constraints, we maintain the diversification from the index.

Takeaways¶

Constraints on the number of assets and total investment in each sector can be incorporated into the model.

Data from pandas DataFrames can easily be used to build an optimization model via the gurobipy-pandas package.

Sums over subsets of the variables can be defined using the DataFrame’s

groupbymethod.