Note

Download this Jupyter notebook and all

data

(unzip next to the ipynb file!).

You will need a Gurobi license to run this notebook, please follow the

license instructions.

Minimum Buy-in¶

The standard mean-variance (Markowitz) portfolio selection model determines an optimal investment portfolio that balances risk and expected return. In this notebook, we minimize the variance (risk) of the portfolio, constraining the expected return to meet a prescribed minimum level. Please refer to the annotated list of references for more background information on portfolio optimization.

To this basic model, we add buy-in thresholds that prevent the investor from holding tiny positions. Holding tiny positions is undesirable because they have a marginal, if any, impact on the expected return but can lead to non-negligible transaction costs, which are not accounted for in the portfolio selection model.

[2]:

import gurobipy as gp

import pandas as pd

import numpy as np

import matplotlib.pyplot as plt

Input Data¶

The following input data is used within the model:

\(S\): set of stocks

\(\mu\): vector of expected returns

\(\Sigma\): PSD variance-covariance matrix

\(\sigma_{ij}\) covariance between returns of assets \(i\) and \(j\)

\(\sigma_{ii}\) variance of return of asset \(i\)

[4]:

# Import some example data set

Sigma = pd.read_pickle("sigma.pkl")

mu = pd.read_pickle("mu.pkl")

Formulation¶

The model minimizes the variance of the portfolio given that the minimum level of expected return is attained and that each position is above a specified lower bound to avoid triggering brokerage costs with tiny positions.

Mathematically, this results in a convex quadratic mixed-integer optimization problem.

Model Parameters¶

We use the following parameters:

\(\bar\mu\): required expected portfolio return

\(\ell > 0\): minimal position size

[5]:

# Values for the model parameters:

r = 0.25 # Required expected return

l = 0.03 # Minimal position size

Decision Variables and Variable Bounds¶

The decision variables in the model are the proportions of capital invested among the considered stocks. The corresponding vector of positions is denoted by \(x\) with its component \(x_i\) denoting the proportion of capital invested in stock \(i\).

We will declare the variables to be semi-continuous, meaning either

Constraints¶

The budget constraint ensures that all capital is invested:

The expected return of the portfolio must be at least \(\bar\mu\):

Objective Function¶

The objective is to minimize the risk of the portfolio, which is measured by its variance:

Using gurobipy, this can be expressed as follows:

[6]:

%%capture

# Create an empty optimization model

m = gp.Model("Portfolio")

# Add variables: x[i] denotes the proportion invested in stock i. Must be greater or equal to l or zero.

# Defining the variable as semi-continuous is enough to enforce the buy-in threshold requirement.

x = m.addMVar(len(mu), lb=l, ub=1, vtype=gp.GRB.SEMICONT, name="x")

# Budget constraint: all investments sum up to 1

m.addConstr(x.sum() == 1, name="Budget_Constraint")

# Lower bound on expected return

m.addConstr(mu.to_numpy() @ x >= r, name="Minimal_Return")

# Define objective function: Minimize risk

m.setObjective(x @ Sigma.to_numpy() @ x, gp.GRB.MINIMIZE)

We now solve the optimization problem:

[7]:

m.optimize()

Gurobi Optimizer version 13.0.2 build v13.0.2rc1 (linux64 - "Ubuntu 24.04.4 LTS")

CPU model: AMD EPYC 7763 64-Core Processor, instruction set [SSE2|AVX|AVX2]

Thread count: 1 physical cores, 2 logical processors, using up to 2 threads

WLS license 2443533 - registered to Gurobi GmbH

Optimize a model with 2 rows, 462 columns and 924 nonzeros (Min)

Model fingerprint: 0x3e0b16ed

Model has 0 linear objective coefficients

Model has 106953 quadratic objective terms

Variable types: 0 continuous, 0 integer (0 binary)

Semi-Variable types: 462 continuous, 0 integer

Coefficient statistics:

Matrix range [7e-02, 1e+00]

Objective range [0e+00, 0e+00]

QObjective range [6e-03, 2e+02]

Bounds range [3e-02, 1e+00]

RHS range [2e-01, 1e+00]

Presolve time: 0.04s

Presolved: 926 rows, 924 columns, 2771 nonzeros

Presolved model has 106953 quadratic objective terms

Variable types: 462 continuous, 462 integer (462 binary)

Found heuristic solution: objective 10.5757854

Root relaxation: objective 2.026597e+00, 154 iterations, 0.01 seconds (0.01 work units)

Nodes | Current Node | Objective Bounds | Work

Expl Unexpl | Obj Depth IntInf | Incumbent BestBd Gap | It/Node Time

0 0 2.02660 0 37 10.57579 2.02660 80.8% - 0s

H 0 0 2.1009626 2.02660 3.54% - 0s

H 0 0 2.0370247 2.02660 0.51% - 0s

H 0 0 2.0344360 2.02660 0.39% - 0s

0 0 2.02660 0 28 2.03444 2.02660 0.39% - 0s

0 0 2.02660 0 28 2.03444 2.02660 0.39% - 0s

0 0 2.02660 0 28 2.03444 2.02660 0.39% - 0s

0 0 2.02666 0 27 2.03444 2.02666 0.38% - 0s

0 0 2.02666 0 27 2.03444 2.02666 0.38% - 0s

0 0 2.02666 0 27 2.03444 2.02666 0.38% - 0s

0 0 2.02666 0 27 2.03444 2.02666 0.38% - 0s

0 0 2.02666 0 27 2.03444 2.02666 0.38% - 0s

0 0 2.02666 0 27 2.03444 2.02666 0.38% - 0s

0 2 2.02666 0 27 2.03444 2.02666 0.38% - 0s

Cutting planes:

MIR: 4

Flow cover: 1

Explored 208 nodes (1161 simplex iterations) in 0.36 seconds (0.28 work units)

Thread count was 2 (of 2 available processors)

Solution count 5: 2.03444 2.03624 2.03702 ... 10.5758

Optimal solution found (tolerance 1.00e-04)

Best objective 2.034435973118e+00, best bound 2.034435973118e+00, gap 0.0000%

We print out the optimal solution and objective value:

[8]:

# Display basic solution data

print(f"Minimum Risk: {m.ObjVal:.6f}")

print(f"Expected return: {mu @ x.X:.6f}")

print(f"Solution time: {m.Runtime:.2f} seconds\n")

# Print investments (with non-negligible value, i.e. >1e-5)

positions = pd.Series(name="Position", data=x.X, index=mu.index)

print(f"Number of trades: {positions[positions > 1e-5].count()}\n")

print(positions[positions > 1e-5])

Minimum Risk: 2.034436

Expected return: 0.250000

Solution time: 0.37 seconds

Number of trades: 23

KR 0.030000

PGR 0.044192

CME 0.030000

ODFL 0.030000

BDX 0.030000

LIN 0.030000

KDP 0.077162

GILD 0.030000

CLX 0.056940

SJM 0.030000

LLY 0.103001

DPZ 0.054447

MKTX 0.030000

MRK 0.036542

ED 0.084887

WST 0.030000

TMUS 0.033931

NOC 0.030000

WM 0.045810

TTWO 0.036782

WMT 0.064940

HRL 0.031366

CPB 0.030000

Name: Position, dtype: float64

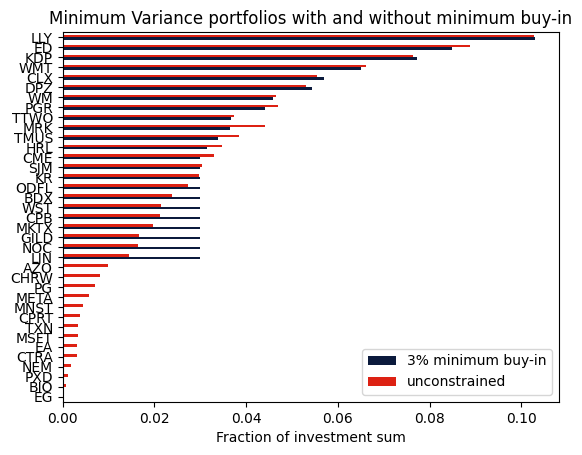

Comparison with the unconstrained portfolio¶

We can also compute the portfolio without the minimum buy-in condition by changing the variable type and bounds of \(x\) and compare the resulting portfolios.

[9]:

# change type of x from semi-continous to continuous

x.vtype = gp.GRB.CONTINUOUS

x.lb = 0

m.params.OutputFlag = 0

m.optimize()

# retrieve and display solution data

mask = (positions > 1e-5) | (x.X > 1e-5)

df = pd.DataFrame(

index=positions[mask].index,

data={

"3% minimum buy-in": positions,

"unconstrained": x.X[mask],

},

).sort_values(by=["3% minimum buy-in", "unconstrained"], ascending=True)

axs = df.plot.barh(color=["#0b1a3c", "#dd2113"])

axs.set_xlabel("Fraction of investment sum")

plt.title("Minimum Variance portfolios with and without minimum buy-in")

plt.show()

Takeaways¶

Semi-continuous variables are decision variables that may either take the value 0 or a value between specified bounds. They are a convenient tool to guarantee a minimum position size for purchased assets.